The 721 Exchange UPREIT Exit Strategy for Delaware Statutory Trust Investors Explained

One of the most important questions Delaware Statutory Trust real estate investors need to ask themselves is, “What is my long-term, exit strategy?”

Most Delaware Statutory Trust (DST) investments are typically held for approximately 5-10 years (although it could be shorter or longer). After that, the DST investment will typically go “Full-Cycle”, a term used to describe a DST property that is purchased on behalf of investors and then after a period of time is sold on behalf of investors.

For more information on the Delaware Statutory Trust full-cycle event, make sure to listen to this informative podcast. While the two most common exit strategies for DST investors include cashing-out and paying taxes or continuing with another 1031 Exchange, Cove Capital Investments can potentially offer investors a third exit option: a 721 UPREIT.

Once your DST investment goes full-cycle, investors need to evaluate what their next investment move should be, including considering the 721/UPREIT option.

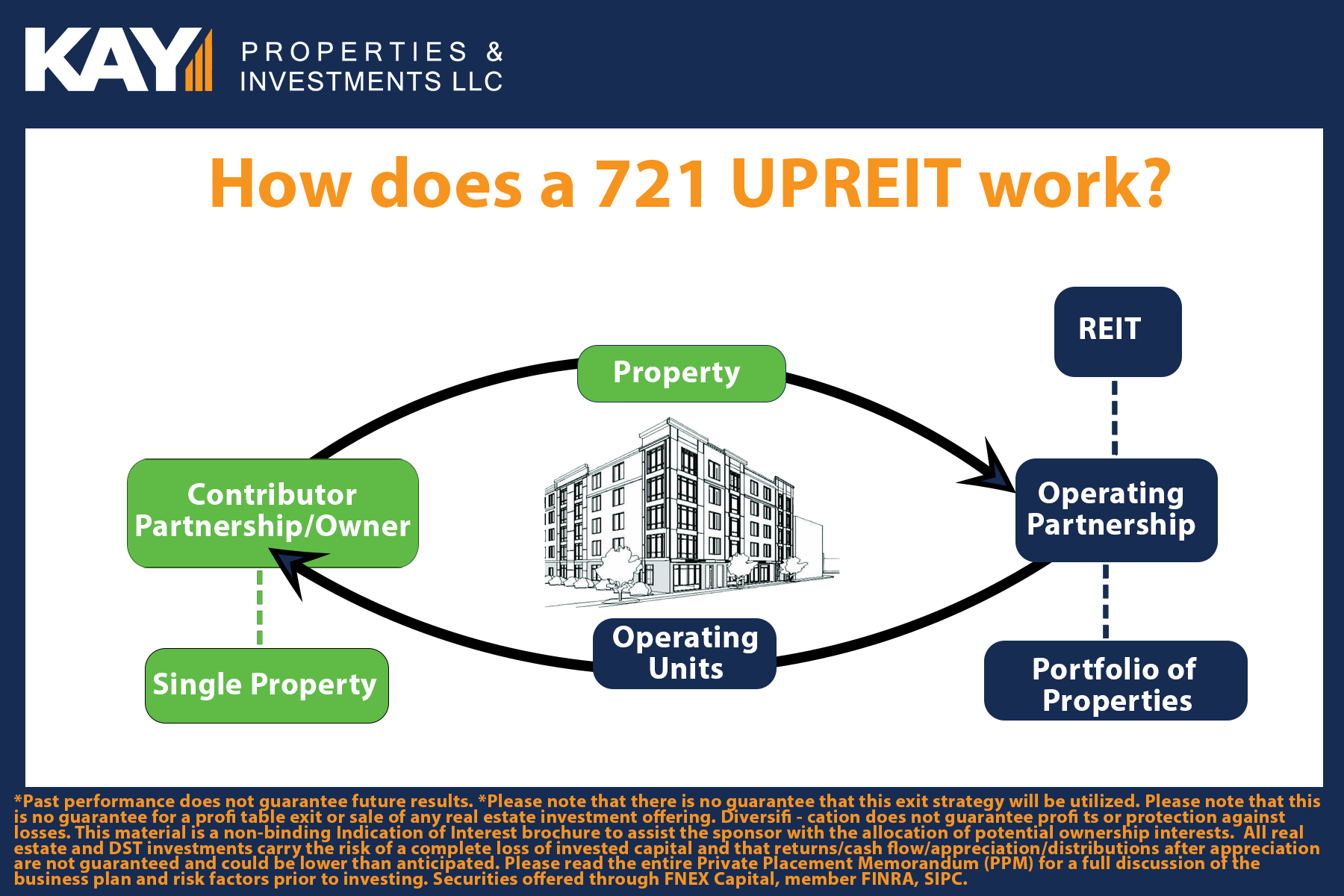

What is a 721 UPREIT Exchange?

The term “UPREIT” is short for Umbrella Partnership Real Estate Investment Trust, which is an operating partnership subsidiary of a REIT that holds and operates real property. Section 721 of the Internal Revenue Code allows owners of real estate property to contribute, on a tax deferred basis, their physical property to a partnership, in exchange for interests in the partnership (a 721 Transaction). This structure allows holders of real estate to exchange real property for economic interest in the REIT in the form of operating partnership units by contributing that property to the partnership in a 721 Transaction. The operating partnership units have economic rights that are identical to the rights of the shares of the REIT, and after a designated holding period can be, if the investor chooses to, converted into shares of the REIT (in a taxable transaction) for liquidity purposes. Investors seeking to defer capital gains taxes while increasing diversification in real estate should consider using a 721 Exchange to realize the following potential benefits.

Tax Advantages - When real estate is typically sold, the investor pays taxes on the capital gains realized as well as depreciation recapture. This leaves the investor with less capital for reinvestment. With the 721 exchange, the investor can avoid this hefty tax through a tax-deferred exchange of appreciated real estate for shares in an operating partnership. These operating partnership units are also known as OP Units. Capital gains can be deferred until the investor sells the OP Units, converts the OP Units to REIT shares, or the contributed property is sold by the acquiring operating partnership.

Diversification - Many investors incur concentration risk by owning one property in a single market. REITs tend to own many assets diversified through different markets. The 721 Transaction into a REIT can provide greater diversification for an individual’s portfolio, which may reduce concentration risk.*

Income Potential - Investors potentially will receive income generated through distributions to the holders of the OP Units.

Liquidity - The ability to convert OP Units of the REIT to shares can provide potential liquidity benefits that are not standard with DST or property ownership. Partial or full liquidity may be achieved, potentially depending on availability determined by the company, by converting the OP Units to shares of the REIT.

Estate Planning - Upon death, shares can be equally split and either held or liquidated by the beneficiaries of the trust. Because these shares are passed through a trust, the beneficiaries receive a step-up basis and can avoid capital gains taxes and depreciation recapture. One Important Caveat for Investors Interested in 721 Exchanges is that REIT shares themselves are not eligible to be used in a 1031 Exchange, and therefore once a 721 Exchange is completed, this is the end of the line for deferral of capital gains taxes. If the shares of the REIT are sold, or the REIT sells a portion of the portfolio and returns the investor’s capital, the investors will be required to recognize any capital gains or loss when they fi le their taxes.